Are we in a bull or bear market for stocks?

- May 25, 2020

- 5 min read

Updated: May 18, 2023

The markets had a particularly bad end of February/March when forced liquidation created a crisis of proportions last seen during the financial crisis. The Central Banks, as usual, stepped in to provide all the liquidity anybody could possibly want, or need, by blowing out their balance sheets to levels never seen before. The result was to calm the financial markets, provide stability and reduce volatility. The US Central Bank (the Fed) in particular has been extremely aggressive stepping up as the buyer of last resort. Central banks have proven time and again, that if there is a liquidity problem, they are more than capable of solving it.

In the meantime, the virus has quietly and expeditiously continued to work its way around the world with its latest victims being in emerging markets where they have less tools to deal with such an event.

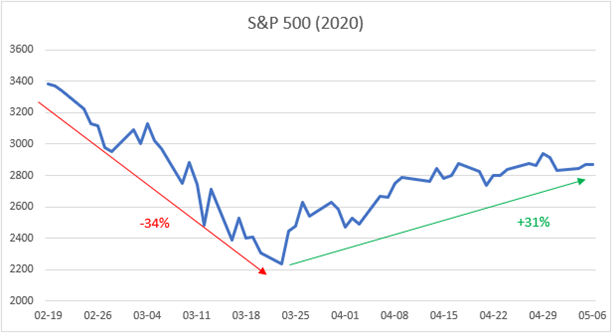

Nevertheless, stock markets have surged, retracing over 60% from the lows of March 23rd as this letter is written. The story is that all the liquidity provided by central banks will help to fill the gap created in the economy by the forced lockdowns around the world to contain the virus. Once it is contained, the story goes, we can go back to normal and resume the upward trajectory of the last decade.

Interestingly, regardless of the circumstances that make markets go down being different, this is exactly the same pattern that can be found in just about every bear market we have witnessed: a big drop anticipating a negative impact on the economy, a retracement when liquidity or some other potential solution comes in to assist, and then lastly, a bigger drop when it is clear that earnings will take more time to come through. In 2008 we also witnessed large retracements on the way to the ultimate low:

We anticipate another drop, just like in previous bear markets such as the one shown above, as it becomes clear that we are in a balance sheet recession which liquidity cannot fix. It can just buy time. Solvency is the issue. The only way to remain solvent is by producing enough cash flow to pay down debt.

Why does this happen every time? Why are people fooled into thinking that this time is different, and that the crisis will be over right away because of one reason or another? It is hard to answer this question other than to say that when it comes to investing, unless you have a deep understanding of the companies you are investing in, and their ability to produce sales and earnings, then hope springs eternal. Not unlike going to Vegas. Either way this is where we are today. After falling 34% the market has retraced well over 60% of the losses since. Although most of the retracement was concentrated in a few tech stocks (with the NASADAQ actually now up for the year), the rest of North American markets are currently down only around 7-15% which is a big improvement from March.

Despite the recent market retracement, we believe we are still in a bear market.

The key today is to try and determine whether this bear market is any different from those of the past. We would argue that it is different this time, because a virus has a bigger structural impact on an economy than a garden variety recession, but the ultimate outcome will be the same. In other words, it is likely that we could get another correction, possibly bigger than the one up to March 23rd, once it becomes clear that the economy is going to take some time to recover to where it was prior to February of this year.

This will be a typical bear market in that we have yet to see the lows before moving higher. Longer term, the prices of companies can only go higher when their earnings grow. This is not in the horizon for 2020 and maybe not even 2021. The fact that stock prices are currently going higher, while the earnings are collapsing, is puzzling to say the least.

This is not a typical recession

This virus is not creating a typical cyclical recession. It is creating a fundamental change in how we work and how we live and while the transition takes place, we have no alternative but to face lower demand in general. Supply chains are being disrupted or relocated locally and that too creates a problem down the road but for now, the lack of demand is the bigger issue. A large part of the economy will have to find employment in new industries as travel and leisure suffers the biggest disruption in over 100 years. This is highly deflationary in nature as lack of demand first and foremost reduces prices.

The economy snapping back quickly is not an option

Although we are confident that a medical solution will be found for the virus, we do not believe it can be produced in large quantities in enough time to make a difference for 2020. At best we are looking at towards the second half of next year before such options are available to the population at large. As such, the economy will not be snapping back fast enough to keep a large part of the population (mainly travel and leisure) employed, and the government must continue to step in to fund the gap.

Economies will reopen. People will get back to work. But in order to avoid trucks or ice rink arenas full of bodies again, some measures will have to be taken in order to deal with the health crisis until there is a medical solution. Many parts of Asia have reopened and people have gone back to work. But on the evenings and weekends, Google mobile data clearly shows that they are not going out very much. And even in Sweden, where the government did not impose a lockdown, people have changed their behaviour as they tried to avoid the virus.

When it comes to your health, most people are smart enough to follow the guidelines proposed by the health experts and scientists and ignore politicians and media pundits who advocate for you going out while they hide in their basements. Social distancing and masks are not conducive to large gatherings or restaurant visits or travelling. This is our new reality for the short to medium term until a medical solution is found.

Any reduction in economic activity (visits to restaurants, functions, travel) is a reduction in GDP and a reduction in cash flow, but the overall debt levels continue to move higher in order to fund the gap. This is a big problem. Collapse in global trade means less cash flows. Collapse in the oil price (not only due to the drop in demand from the pandemic but also an ill timed price war by the Saudis and the Russians), means less cash flows for that industry. That is a problem, especially for oil producing economies such as Canada. Less tax revenues as businesses remain shut is a problem. All of these lead to the inability to service higher than normal debt levels for corporations, who have to finance the gap, the consumer who has to use their savings, if they have any, while not working, and the government who has to fund its own revenue gap (from lower tax revenue) plus try and assist everybody else.

As central banks have piled in with a lot of cash to fill in the demand gap and try and keep people employed, there is the thought that as soon as medical solution is found, the economy will snap right back. Unfortunately, snapping back is likely to be more sluggish than expected as it will take time. It is also likely to be slower than we want because we went into this crisis ill prepared financially, by having too much debt, and the crisis is just adding to that problem.

It is said that bear markets are not over until they have made a fool out of everybody. It is likely the markets can continue to rally into the summer and even the fall, until the virus re-merges or the realization that this is not going to be a normal recession finally kicks in. Portfolios need to be positioned accordingly.

The Summerhill Team

Comments